How hidden inefficiencies were costing one lender over $300k annually, and how data-driven changes fixed them

Introduction

Here's something we hear a lot: 'We've always done it this way.' And honestly? Sometimes that's fine."

When a leading mortgage lender partnered with Certified Credit, their credit reporting operations seemed efficient on the surface. But a deeper analysis revealed substantial opportunities hidden in their data.

Through comprehensive peer benchmarking and transparent reporting, we uncovered inefficiencies that were costing them hundreds of thousands of dollars annually. The solution didn't require expensive new technology or a complete operational overhaul—just strategic adjustments based on data-driven insights.

Here's what we helped them achieve:

- 50% reduction in prequalification volume without sacrificing application quality

- 20% improvement in prequal pull-through rates

- 85% reduction in supplement orders through smarter verification processes

- 15% reduction in average loan cost

- $20,000 to $25,000 in monthly savings

This case study walks through how transparent data analysis transformed their operations and delivered measurable, sustainable results.

Download Case Study

The Challenge

Like many mortgage lenders, this client had established credit reporting processes in place for years. Without comprehensive data analysis and peer benchmarking, several significant inefficiencies had gone unnoticed. Inefficiencies that were quietly draining their budget month after month.

Excessive Prequalification Volume

The client was pulling over 1,200 soft credit inquiries monthly for prequalification purposes. While prequalification serves an important role in the lending process, a detailed analysis revealed a striking inefficiency: 75% of these applicants already had credit scores above 720, well within acceptable lending parameters for most loan products.

This meant the majority of prequalifications were unnecessary, consuming valuable resources and budget without adding meaningful value to lending decisions. The client was essentially paying to confirm information about borrowers' creditworthiness that they could reasonably infer from initial application data.

Inefficient Supplement Ordering Process

The second major challenge involved supplement ordering practices. The client was ordering supplements on 30% of all hard credit pulls, a rate significantly higher than industry benchmarks. These supplements represented substantial additional costs and extended processing timelines.

Detailed investigation revealed that nearly 80% of these supplement requests were simple Verification of Mortgage (VOM) inquiries. These types of verifications are typically handled efficiently by automated systems and can often be satisfied by standard mortgage statements. However, the client had defaulted to ordering manual supplements rather than accepting readily available documentation, creating unnecessary expenses and delays.

Limited Visibility Into Performance Patterns

The most fundamental challenge was visibility. Without detailed reporting on prequalification effectiveness, supplement usage by type, and peer comparison data, the client had no way to identify these inefficiencies or measure the potential impact of process improvements on conversion rates and cost per loan.

They needed more than credit reports. They needed actionable intelligence to drive strategic decision-making.

Solution

Certified Credit approached this engagement as a strategic partnership, implementing a comprehensive data analysis and reporting solution designed to provide unprecedented visibility into credit reporting processes and clear pathways to optimization.

In-Depth Peer Analysis and Benchmarking

We conducted extensive peer analysis to benchmark the client's processes against industry standards and best practices from similar lenders. This comparative approach revealed specific areas where the client's practices diverged from more efficient models, particularly in prequalification thresholds and supplement ordering protocols.

Rather than simply identifying differences, we analyzed the business impact of these variations and quantified potential savings. This gave the client's leadership team concrete data to support process changes, moving beyond anecdotal evidence to data-driven decision-making.

Comprehensive Transparent Reporting

We established a transparent reporting system that tracked critical performance indicators:

- Monthly prequalification volume and pull-through rates

- Hard pull-to-close conversion rates

- Supplement ordering frequency by type

- Average cost per loan with monthly trending

- Hard-pull-to-refresh tracking for credit management

This data was regularly shared with the client's leadership team through detailed monthly reports and executive summaries, enabling informed decision-making and highlighting opportunities for improvement. The transparency of this reporting built trust and created a foundation for collaborative problem-solving.

Strategic Process Recommendations

Based on comprehensive analysis and peer benchmarking, we recommended two strategic process changes, each supported by detailed cost-benefit analysis:

- Strategic Prequalification Threshold Adjustment

We recommended implementing more strategic prequalification criteria to eliminate unnecessary soft pulls for applicants with strong credit profiles. Since 75% of applicants had credit scores above 720, we suggested these individuals could proceed directly to the application stage, reserving prequalifications for borderline credit situations where they add genuine value to the lending decision.

This approach would reduce costs while improving the customer experience by streamlining the process for qualified borrowers.

- Statement Acceptance for Routine VOM Requests

We identified significant savings opportunities if the client accepted standard mortgage statements for routine verification needs rather than automatically ordering costly manual supplements. This recommendation specifically targeted the 80% of supplements that were simple VOM requests, situations where existing documentation could satisfy verification requirements.

We provided clear guidelines on when supplements were truly necessary versus when standard statements would suffice, along with quality assurance protocols to ensure compliance requirements remained fully met.

Outcome

The implementation of these data-driven recommendations delivered substantial, measurable results that exceeded expectations. The transformation represented a fundamental improvement in operational efficiency with lasting impact.

Prequalification Optimization

50% reduction in prequalification volume. By adjusting prequalification thresholds, the client reduced monthly soft pulls from over 1,200 in April to 615 by September. This dramatic reduction eliminated unnecessary credit inquiries while maintaining application quality and customer satisfaction.

20% improvement in prequal pull-through rates. The more targeted prequalification approach resulted in better conversion quality. Pull-through rates improved from 23.19% in April to 27.97% in September, demonstrating that strategic focus on high-value prequalifications delivered superior results.

Enhanced Conversion Metrics

10% increase in hard-pull-to-close rate. Combined with in-depth hard-pull-to-refresh tracking, the process adjustments contributed to measurable improvement in the overall hard-pull-to-close conversion rate, indicating better-quality applicants and more efficient processing throughout the pipeline.

Dramatic Supplement Reduction

From 30% to under 5% supplemented hard pulls. Following implementation of recommendations to accept statements for routine VOM requests, the percentage of hard pulls requiring supplements dropped from 30.59% in April to just 4.54% in September… an 85% reduction!

$5,000 in additional monthly savings. The supplement reduction alone saved the client $5,000 per month in direct credit reporting costs, while simultaneously streamlining the loan process and reducing turnaround times.

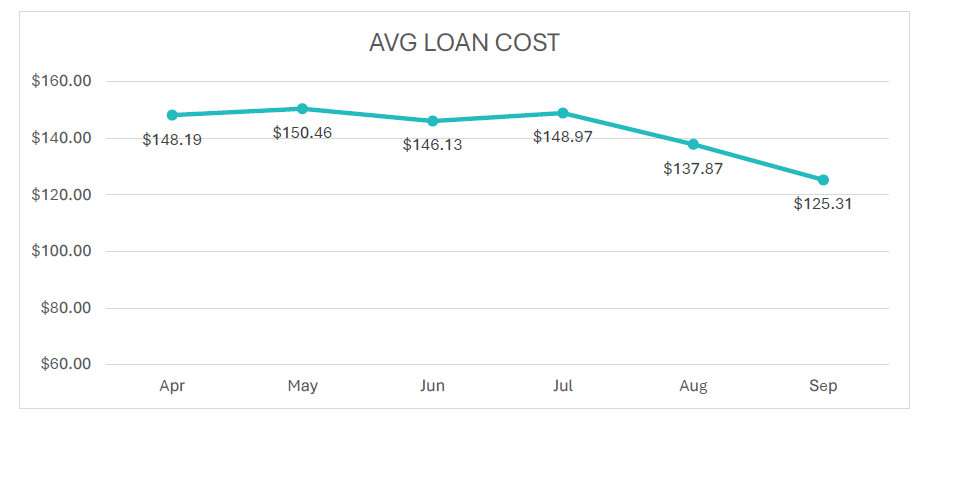

Overall Cost Reduction

15% reduction in average loan cost. The combined efficiency gains reduced the client's average loan cost with Certified Credit by 15%, declining from $148.19 in April to $125.31 in September, a consistent downward trend reflecting sustained process improvements.

$20,000 to $25,000 in monthly savings. These operational improvements resulted in monthly savings of $20,000 to $25,000, representing significant reductions in credit reporting expenses without compromising loan quality, compliance standards, or applicant experience.

Download Case Study

Performance Transformation: April to September

The following table summarizes the measurable transformation in key performance indicators:

Download Case Study

What Sets Us Apart

This success story illustrates several key differentiators that define the Certified Credit approach:

Partnership Over Transactions

While many credit reporting companies focus solely on delivering reports, Certified Credit operates as a strategic partner invested in client success. We provide actionable insights that drive business improvements, understanding that when our clients succeed, we succeed. This engagement demonstrates our commitment to understanding unique challenges and working collaboratively to solve them, even when recommendations reduce service usage, as evidenced by the prequalification reduction.

Transparency as a Core Value

Transparency builds trust and enables better decision-making. Our comprehensive reporting extends far beyond basic transaction records to provide detailed analytics, peer comparisons, and trend analysis. We share everything clients need to evaluate their performance and identify opportunities, believing that informed clients make better decisions.

Data-Driven Recommendations

Every recommendation is backed by comprehensive data analysis and peer benchmarking. We quantify the potential impact of process changes before implementation and track results meticulously afterward, giving clients confidence that decisions are based on solid evidence rather than assumptions or industry trends.

Industry Expertise and Education

Our team brings deep expertise in mortgage credit reporting, compliance requirements, and industry best practices. Beyond making recommendations, we educate clients on why certain approaches work better than others, empowering them to make strategic decisions that align with their business objectives and risk tolerance.

Continuous Improvement Focus

This case study represents one six-month engagement, but our commitment to client success is ongoing. We continuously monitor performance metrics, identify new opportunities for optimization, and proactively share insights. The relationship extends far beyond report delivery—that's where the partnership truly begins.

More Than Just a Score

Certified Credit is redefining credit reporting partnerships in the mortgage industry by combining comprehensive tri-merge reports, strategic prequalification services, and intelligent verification solutions with transparent data analytics that drive real business results.

Our platform integrates seamlessly with major loan origination systems, while our team serves as trusted advisors who proactively identify cost-saving opportunities and process improvements. Whether you're a small independent lender or a large national operation, we have the expertise, technology, and commitment to help you achieve measurable results like those detailed in this case study.